What Is One Medicare Advantage Client Worth Over 5 Years?

# What Is One Medicare Advantage Client Worth Over 5 Years?

Most agents think about Medicare Advantage in terms of what one sale pays. That's the wrong frame. The right question is what one client pays over the years they stay with you — and that number changes everything about how you run your business.

The 2026 Commission Numbers You Need to Know

CMS raised Medicare Advantage broker compensation caps for 2026. The new national maximum is $694 for an initial enrollment and $347 per year for renewals.

That's a meaningful increase from 2025 rates of $611 and $306. Carriers don't have to pay the max — but most competitive carriers do to attract top producers.

These numbers are the foundation of every LTV calculation you'll do.

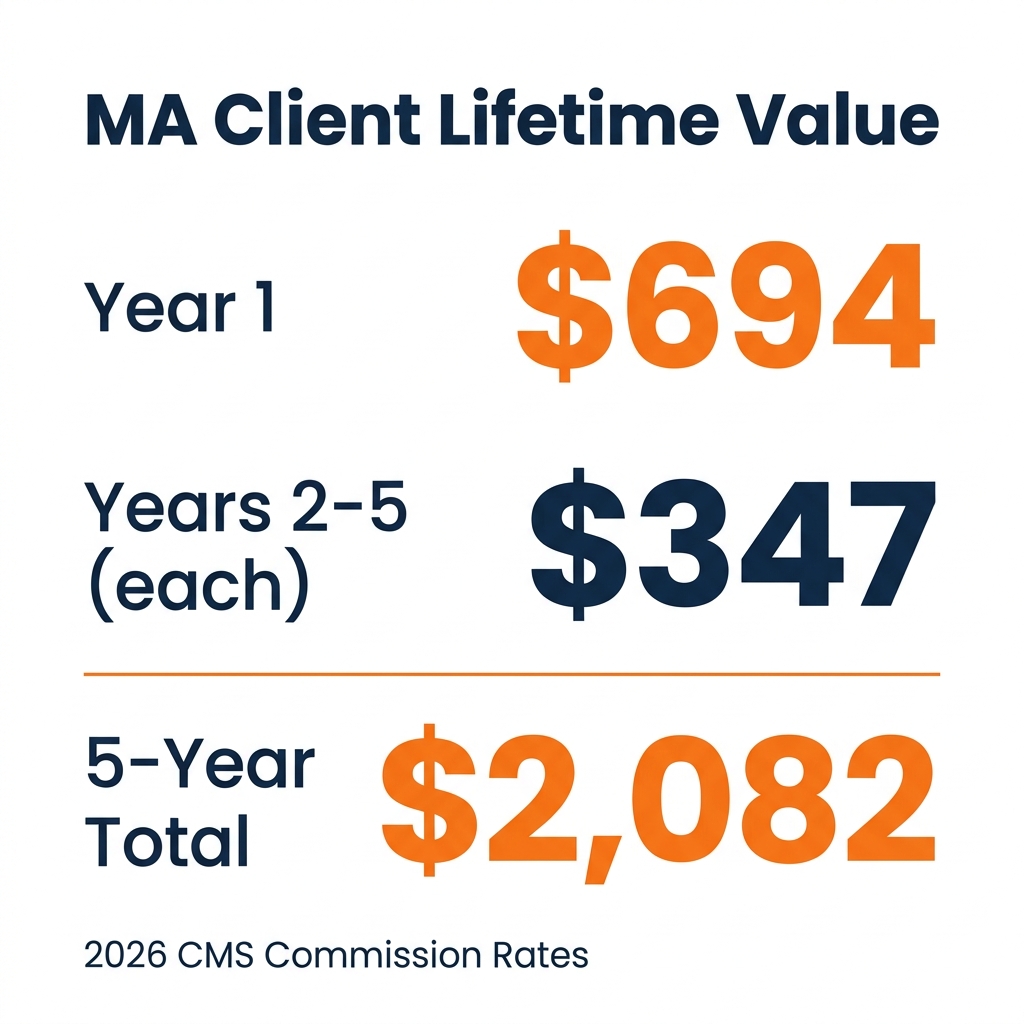

The 5-Year Math on One Client

Here's what a single Medicare Advantage client is worth if they stay with you for five years:

- Year 1: $694

- Year 2: $347

- Year 3: $347

- Year 4: $347

- Year 5: $347

Total: $2,082 from one client over five years.

That assumes no plan switches, no cross-sells, and no referrals. It's the floor — not the ceiling.

At ten years, that same client has paid you $3,817. And you did the work once.

Why Retention Is the Real Lever

Most agents focus on getting the next lead. The highest-earning agents focus on keeping the clients they already have.

The math is simple. An agent with 100 active MA clients earns roughly $34,700 per year in renewals alone — before writing a single new policy. That's a base income that grows every time they add a client.

Average MA client retention runs 6 to 7 years. Some clients stay 10 to 15 years if you serve them well. Every year of retention you add is worth $347 per client.

A 10% improvement in retention across 100 clients is $3,470 per year in additional income — for doing nothing extra except staying in touch.

The Cross-Sell Layer: Where LTV Doubles

MA commissions are just the start. Most Medicare clients also need:

- Hospital indemnity — fills gaps in MA coverage

- Dental, vision, hearing — many MA plans have weak ancillary coverage

- Final expense (FE) — natural cross-sell once trust is established

- Life insurance or annuities — for clients with assets to protect

Note: Non-health products like FE and life insurance must be sold in separate appointments from Medicare plan discussions. CMS rules prohibit combining them.

When agents cross-sell effectively, LTV per client easily doubles. An MA client who also has an FE policy and a hospital indemnity plan can be worth $4,000 to $5,000 over five years — from a single acquisition.

Agents earning $200k or more typically offer six or more products per household. They're not working more leads. They're earning more per relationship.

What This Means for Your Lead Cost

If one MA client is worth $2,082 over five years, what should you be willing to spend to get that client?

Run the math. A campaign that delivers appointments at a $35 cost per lead, with a 22% book rate and 30% close rate, produces a client for roughly $530 in total acquisition cost.

$530 to acquire a $2,082 client. That's a 3.9x return — before cross-sells and referrals.

Most agents who complain about lead cost are thinking about the $35 CPL. The ones who scale think about the $2,082 LTV. Same data, completely different business.

Our 90-Day Medicare Appointment Sprint is built around this exact math. We target a $35 CPL and guarantee 25 qualified appointments in 90 days — or we keep working until you get them. At a 30% close rate, that's 7 to 8 new MA clients with $14,000 to $17,000 in projected 5-year LTV each. [Learn more about the Sprint →]

The Compounding Effect Most Agents Miss

Here's what most agents don't account for: referrals.

A satisfied MA client who's been with you for three years has a network. They talk to their friends at the senior center, at church, at family dinners. A single referred client from a loyal existing client costs you nothing in acquisition.

That referred client brings another $2,082 in five-year LTV. Multiply that across even a handful of referrals per year and you start to see why top Medicare agents stop buying leads entirely after a few years of building a good book.

The pipeline pays for itself. That's the business model.

Ready to Build a Book That Compounds?

Understanding LTV changes how you think about every appointment, every lead, and every client you serve. If you're still treating Medicare sales as a one-time transaction, you're leaving most of the income on the table.

Want to see what a real Medicare appointment pipeline looks like?

Book a free 20-minute strategy call. We'll look at your current lead flow, show you what we'd change, and give you a realistic picture of what consistent appointments could look like for your market — no pitch, no obligation.

[Book Your Free Strategy Call →]

Frequently Asked Questions

Q: How much does a Medicare Advantage client pay an agent over 5 years? A: At 2026 commission rates, an MA client is worth $694 in year one and $347 per year after that. Over five years, that's $2,082 per client — before cross-sells or referrals. At 10 years, the total reaches $3,817.

Q: What are Medicare Advantage renewal commissions in 2026? A: CMS set the 2026 national maximum MA renewal commission at $347 per year. This is paid each year the client stays enrolled in their plan, as long as you remain their agent of record. Rates vary slightly by state.

Q: How do Medicare agents increase income per client? A: The biggest lever is cross-selling. Agents who add hospital indemnity, dental/vision, and final expense to their MA clients double or triple their LTV per household. Retention is the second lever — every additional year a client stays is worth $347.

Q: Can Medicare agents sell final expense at the same appointment as Medicare? A: No. CMS rules prohibit selling non-health products (FE, life, annuities) in the same appointment as Medicare plan discussions. Cross-selling must happen in a separate, scheduled appointment after the Medicare conversation is complete.