The Medicare Cross-Sell Map: MA to FE to Life to Annuity

Most carriers cut Part D commissions to zero for 2026. Agents who built their income around Medicare Advantage plus PDP are now seeing a gap in every renewal. The answer isn't finding a new lead source. It's earning more from the clients you already have.

Why Cross-Selling Is No Longer Optional

A Medicare Advantage client at 2026 commission rates pays you $694 in year one and $347 per year after that. That's strong — but it's one product in a household that likely needs four or five.

Agents earning $150k to $200k+ are not writing twice as many MA plans. They're writing the same volume and cross-selling 2 to 3 additional products per household. With Part D commissions gone, cross-selling isn't a growth strategy — it's income protection.

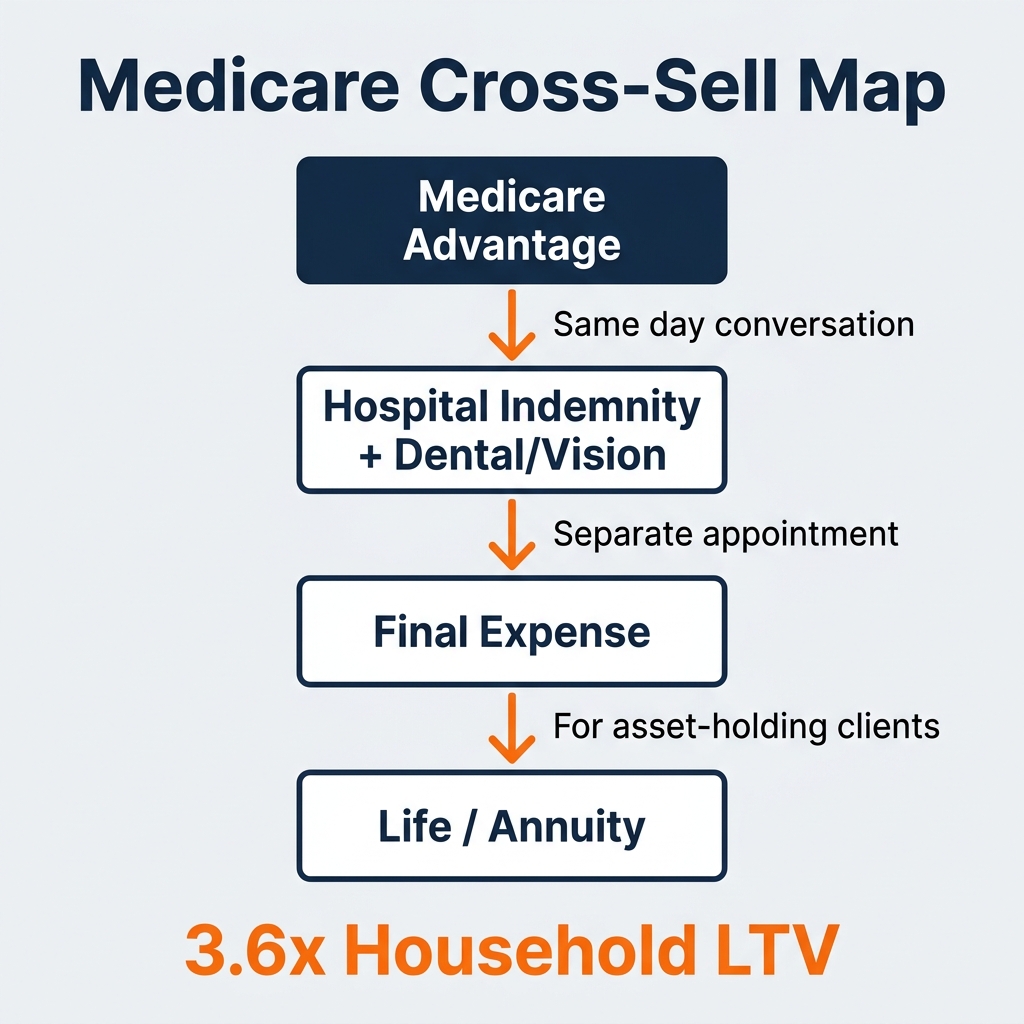

The Medicare Cross-Sell Map

Layer 1: Ancillary health products

- Hospital Indemnity — pays a lump sum for hospital stays MA doesn't fully cover

- Dental / Vision / Hearing — fills gaps most MA plans leave open

- Cancer / Critical Illness — relevant for clients with health concerns

Layer 2: Final Expense life insurance (separate appointment required)

- The average funeral costs $8,000 to $12,000. Most Medicare clients have no coverage.

- Year 1 commission: 50 to 120% of annual premium (carrier dependent)

- Renewals: 5 to 10% annually

- Easiest conversation because the need is obvious and universal

Layer 3: Life insurance and annuities (for asset-holding clients)

- Life insurance for clients with a spouse, home, or dependents

- Annuities for clients with IRA/pension money seeking guaranteed income

- Commissions: 4 to 8% of annuity premium; varies for life

- Requires additional licensing in most states

The Compliance Line You Cannot Cross

CMS rules prohibit discussing non-health products during a Medicare sales appointment. Final expense, life, and annuities must happen in a separate, scheduled appointment — not the same meeting as the MA enrollment.

Schedule the cross-sell conversation immediately after enrollment: "While we're wrapping up, I'd love to spend 20 minutes next week reviewing the rest of your coverage picture." Most clients say yes. The hard part is remembering to ask.

What the Math Looks Like Per Household

- MA 5-year LTV: $2,082

- Final Expense 5-year LTV: ~$1,000

- Hospital Indemnity 5-year LTV: ~$540

- Total household 5-year LTV: $3,622

From one acquisition. All you changed was the number of conversations you had with a client who already trusts you.

When to Have the Cross-Sell Conversation

Right after MA enrollment, before the client hangs up: "I want to make sure we've looked at your full coverage picture. Do you have any life insurance or final expense coverage in place? Would it be okay if I spent 20 minutes with you next week walking through the rest?"

Build this into your GHL workflow — after every MA enrollment, a task triggers: "Schedule cross-sell appointment — FE and HI." Automate the ask so you never forget.

Want to see what a real Medicare appointment pipeline looks like?

Book a free 20-minute strategy call. We'll look at your current lead flow, show you what we'd change, and give you a realistic picture of what consistent appointments could look like for your market — no pitch, no obligation.

[Book Your Free Strategy Call →]

Frequently Asked Questions

Q: Can you sell final expense at the same appointment as Medicare? A: No. CMS rules prohibit selling or discussing non-health products — including final expense, life insurance, and annuities — during a Medicare plan appointment. Cross-selling must happen in a separate, scheduled meeting.

Q: What is the best product to cross-sell to Medicare Advantage clients? A: Final expense life insurance is typically the most natural and highest-commission cross-sell. The need is universal and the conversation is easy to open. Hospital indemnity is the second most natural fit, covering gaps MA leaves open.

Q: How much more income can agents make by cross-selling? A: An MA client with a final expense policy and hospital indemnity plan can generate 70 to 80% more five-year LTV than an MA-only client. Agents with an active cross-sell program typically earn $40k to $80k more per year.

Q: Do I need extra licenses to cross-sell to Medicare clients? A: For hospital indemnity and dental/vision — typically no, if you already hold your health license. For final expense and whole life — you need a life insurance license. For annuities — you need a life license plus annuity certification in most states.