First Year as a Medicare Agent: What It Actually Looks Like

Your first year as a Medicare agent is not what the recruiter promised. The pitch is six figures by Year 2 and freedom by Year 3. The reality is licensing fees, FMO releases, leads that go nowhere, and an income curve that climbs much slower than expected.

This post is the honest version. What you actually earn. What you actually do. Where the leads come from. And what separates the agents who hit Year 2 from the agents who quit before AEP.

What a Realistic First Year as a Medicare Agent Earns

The income range in Year 1 is wide. Industry data and agent forums paint a clear picture: most new agents earn around $30,000 in their first year. Top performers can clear $100,000. The national average across all Medicare agents (including 5+ year veterans) is around $76,890.

The gap between $30,000 and $100,000 is not luck. It is volume, lead source, and follow-up discipline. A new agent who writes 30 Medicare Advantage policies in their first year is making $20,820 in MA commissions alone (30 × $694 Year 1 commission for 2026). Add cross-sell, PDP, and Final Expense, and that climbs to $30,000 to $40,000.

A new agent who writes 100 policies clears $69,400 in MA commissions before any cross-sell. The math is simple. The execution is what splits the field.

Why Year 1 Income Is Lower Than the Pitch

Three things compress Year 1 income. The first is licensing time. State exam, AHIP certification, carrier contracting, and FMO onboarding take 30 to 90 days. You cannot legally write a policy until all of it is done.

The second is renewal lag. Renewals do not start paying until Year 2. Your entire Year 1 income is initial commission only — no recurring revenue from renewals yet.

The third is lead cost. New agents spend more per lead than experienced agents because they have not built referral pipelines yet. They pay vendors, buy from FMOs, or run untested ads. The cost-to-acquire is higher than it will be in Year 3.

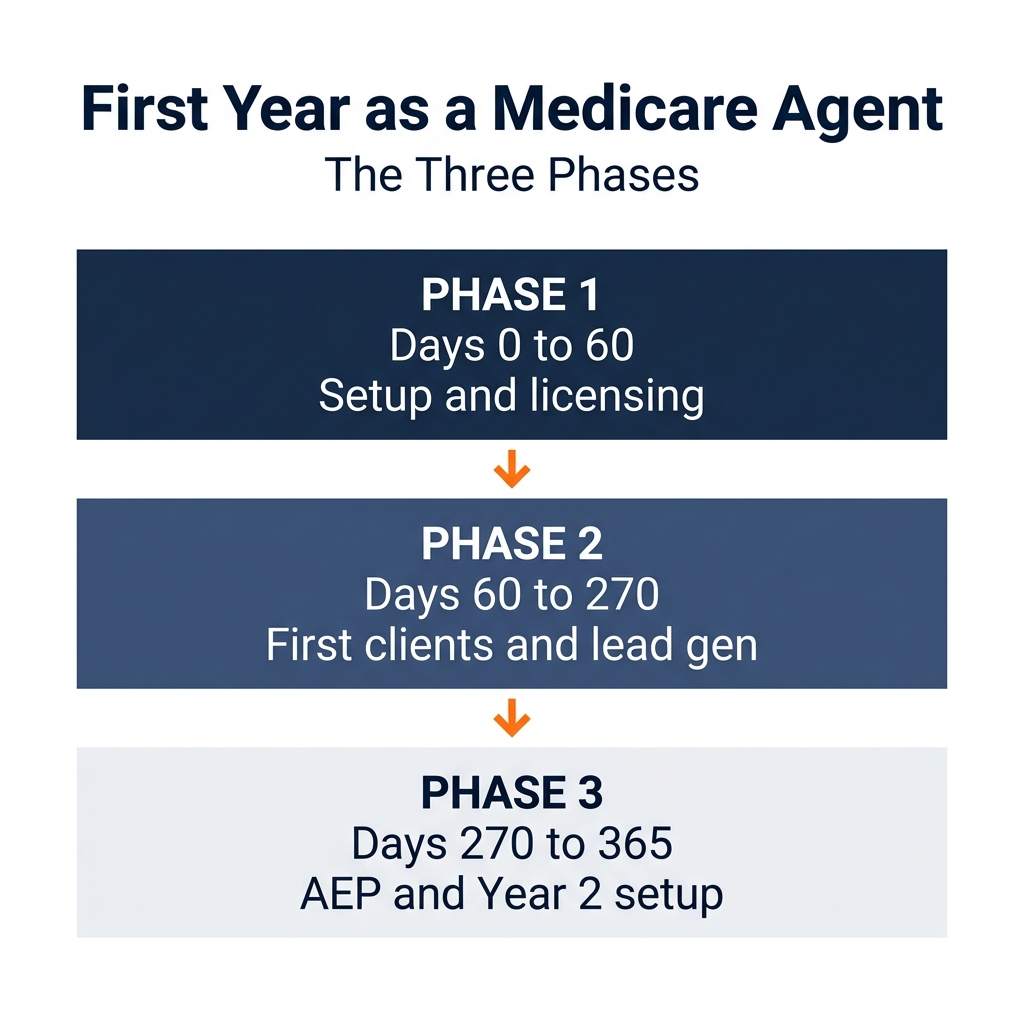

What You Actually Do in Your First Year as a Medicare Agent

The first year breaks into three phases. Most agents underestimate the first phase and skip the third.

Phase 1 (Days 0 to 60): Setup. You finish your license, take AHIP, contract with 3 to 5 carriers, choose an FMO, and set up E&O insurance. Costs run $500 to $1,500 depending on state and FMO setup. No income yet.

Phase 2 (Days 60 to 270): First clients. You start writing policies. Most agents find their first 5 clients through warm market — friends, family, prior coworkers. Then they need a real lead source. This is where the income curve splits between agents who figure out lead generation and agents who do not.

Phase 3 (Days 270 to 365): Setting up Year 2. AEP hits in mid-October. Agents who built a process in Phase 2 ride AEP. Agents who did not are working overtime to make up for 9 months of soft pipeline. The agents who hit Year 2 build cross-sell and referral systems in this final phase.

The FMO Trap Most New Agents Walk Into

Almost every new Medicare agent signs with a Field Marketing Organization (FMO) in Phase 1. FMOs offer "free" leads, training, and carrier contracts. The trade-off is rarely explained upfront.

When you contract through an FMO, you are typically locked in for 90 days. If you want to leave, you either wait the full 90 days or get a written release from the FMO. During those 90 days, the FMO can pause your access to digital systems, marketing capital, or even your own commission flow.

The fix is not to skip FMOs. It is to read the contract before signing. Look for the release policy. Look for the lead-cost terms. Pick an FMO that treats you like a partner, not a captive audience.

Where New Medicare Agent Leads Actually Come From

The recruiter showed you a deck full of "free leads." The reality is that almost every Medicare agent eventually pays for leads in some form, including the ones who say they "only do referrals."

The 5 lead sources every new agent considers in their first year:

- Warm market — friends, family, neighbors. Free but limited. Tap out by month 3.

- Referrals from existing clients — the cheapest long-term lead source, but you need clients first.

- FMO-provided leads — usually shared, often aged, sometimes recycled. Cheap on price, expensive on contact rate.

- Direct mail — slow, expensive per lead, but works if you have a budget and patience.

- Paid digital ads (Facebook, Google) — the highest control, the steepest learning curve.

Most new agents bounce around all 5 in Year 1. They start with warm market, run out, try FMO leads, get burned by low contact rates, dabble in mail, then either give up or commit to a real ad strategy.

The Lead Quality Trap

The single most expensive Year 1 mistake is buying cheap leads. A $5 shared Medicare lead sounds great until you realize it is also being sold to 9 other agents. Contact rates on shared leads run around 10 to 15%. You are paying $5 for a 1-in-7 chance the prospect even picks up.

A $50 exclusive lead with an SMS confirmation has a contact rate above 80% because the prospect actually wants to talk to you. The math always favors lead quality over lead price for a new agent who cannot afford to waste time.

This is exactly the trap our 30-Day Lead Sprint solves. We deliver 25 exclusive, SMS-verified, T-65 leads in 30 days — never shared, real-time, fully integrated with your CRM. For new agents, it is the fastest way to bypass the shared-lead trap. Learn more about the Sprint here.

What Separates the Agents Who Survive Year 1 From the Ones Who Do Not

Three habits show up in every successful first-year agent. They are simple, free, and most agents skip them anyway.

Habit 1: Track every lead. Even if your "CRM" is a spreadsheet in month one, track every prospect, every conversation, every status. The agents who scale in Year 2 already had organized client data in month 6.

Habit 2: Run a 5-minute response window. When a lead comes in, contact them within 5 minutes. The data is consistent across every industry: 5-minute response triples your contact rate vs 1-hour response. New agents lose more deals to slow follow-up than to bad leads.

Habit 3: Annual review every client from month 1. Even your first 5 warm-market clients should get an annual review. This is what creates referrals. Referral pipelines start in Year 1, not Year 3.

What to Expect in Year 2 (If You Survive Year 1)

Year 2 income jumps for two reasons. Renewals start paying ($347 per active MA client at the 2026 rate). And your client base is now large enough to generate real referrals.

A first-year agent who wrote 50 MA clients walks into Year 2 with roughly 45 active clients (90% retention). 45 × $347 = $15,615 in renewal income before they write a single new policy. Stack that on top of new sales and Year 2 income often doubles Year 1.

The agents who get to Year 2 do not work harder. They built systems in Year 1 that compound in Year 2. See the full 3-lever Medicare agency scaling system here. That is the entire game.

The First Year as a Medicare Agent Comes Down to Lead Quality

Most of what you read about being a new Medicare agent focuses on the wrong things. Carrier contracts and AHIP scores matter, but only after you can put real prospects in your CRM.

Lead quality is the single biggest variable in your first year. The agents who solve it early hit Year 2. The agents who chase $5 shared leads work twice as hard for half the result. Decide which agent you are going to be in month 1, not month 11.

Want to see exactly how new Medicare agents get to 25 exclusive T-65 leads in their first 30 days?

We put together a short video that walks through the whole system. How the leads are generated, how they are qualified, and what happens after they hit your CRM.

Or if you are ready to talk now, book a free 20-minute strategy call here. No pitch. Just a look at your market and what consistent leads could look like.

Frequently Asked Questions

Q: How much does a first-year Medicare agent make?

A: Most new Medicare agents earn around $30,000 in their first year. Top performers clear $100,000+ depending on volume and lead source. The first year as a Medicare agent is built almost entirely on initial commissions ($694 per MA enrollment in 2026) since renewals do not start paying until Year 2.

Q: What is the first year as a Medicare agent really like?

A: The first year breaks into three phases: setup (days 0-60: license, AHIP, FMO contracts), first clients (days 60-270: warm market, then real lead generation), and AEP plus Year 2 setup (days 270-365). Most agents underestimate Phase 2 and run out of warm-market leads by month 3.

Q: Where do new Medicare agents get leads?

A: New Medicare agent leads come from 5 main sources: warm market, referrals, FMO-provided leads, direct mail, and paid digital ads. Most new agents start with warm market and FMO leads but eventually need exclusive paid lead generation to scale beyond the first 20-30 clients.

Q: Do new Medicare agents need an FMO?

A: Most new Medicare agents work with a Field Marketing Organization (FMO) for carrier contracts, training, and certification support. Watch the contract terms — most FMOs lock you in for a 90-day period, and during that window the FMO controls your access to systems and lead capital. Read the release policy before signing.