Independent vs Captive Medicare Agent Income Year 3

Independent vs captive Medicare agent income looks the same in year 1. By year 3 it's a different business. The gap isn't about commission rates. It's about who owns the book.

Most agents leave a captive role because they want more control. The income decision is harder than it looks. The math below shows what year 3 actually looks like for both paths.

Independent vs Captive Medicare Agent Income: Why Year 3 Is the Real Test

Year 1 favors captive agents. They have a base salary, leads handed to them, and a built-in support team. An independent agent in year 1 is paying for their own CRM, leads, and E&O insurance.

Year 3 flips it. The captive agent's renewal stack is capped or owned by the company. The independent agent's renewal stack belongs to them and compounds every year.

This is why the income comparison only makes sense over a 3 to 5 year window. Anything shorter hides the real story.

How Captive Medicare Agents Get Paid

A captive Medicare agent works for one carrier or one agency. The company pays them a base salary plus a reduced commission per enrollment. The trade is simple: stability now, in exchange for less upside later.

Salary + Reduced Commission

Captive agents typically earn 33% to 50% less per enrollment than independents. The carrier or parent agency keeps that difference to fund the support layer.

To make the comparison concrete, this post will use a captive rate of around $450 per Medicare Advantage enrollment in year 1. That's a representative figure based on the 33% to 50% gap reported across captive contracts. Renewals in this scenario run about $225 per active client per year.

The base salary in this scenario is $30,000. Some captive shops pay more. Some pay less. Some pay zero base and only a draw against commissions.

Who Owns the Book

This is the line that decides everything.

In most captive contracts, the agency or carrier owns the book of business. When the agent leaves, the renewals stay with the company. The agent walks away from the income they spent years building.

That's the hidden cost of the captive model. The renewal income looks great while you're employed. It disappears the day you resign.

How Independent Medicare Agents Get Paid

An independent Medicare agent contracts directly with multiple carriers through an FMO. They get the full street level commission. They own every client they write.

Street Level Commissions Through an FMO

The maximum CMS-allowed commission for a Medicare Advantage enrollment is around $694 in year 1. Renewals are about $347 per active client per year. Independent agents at street level earn that full rate.

An FMO contract gives the same commission level the carrier would pay direct. The FMO makes its money on overrides from the carrier, not from cutting your commission. That's the structural advantage.

Renewals That Compound

Renewals are where the independent agent income story is built.

Every Medicare Advantage client written in year 1 pays a renewal in year 2, year 3, and beyond as long as they stay enrolled. A 5-year LTV per client works out to $694 + (4 × $347) = $2,082 per active MA client.

By year 3, the agent has three layers stacking: new business from year 3, plus renewals from year 1 and year 2. That's the compounding the captive model doesn't replicate.

The Year 3 Income Math: Independent vs Captive Medicare Agent Income Side-By-Side

To make the math concrete, this section compares two agents. Both write 100 Medicare Advantage enrollments per year. One is captive. One is independent.

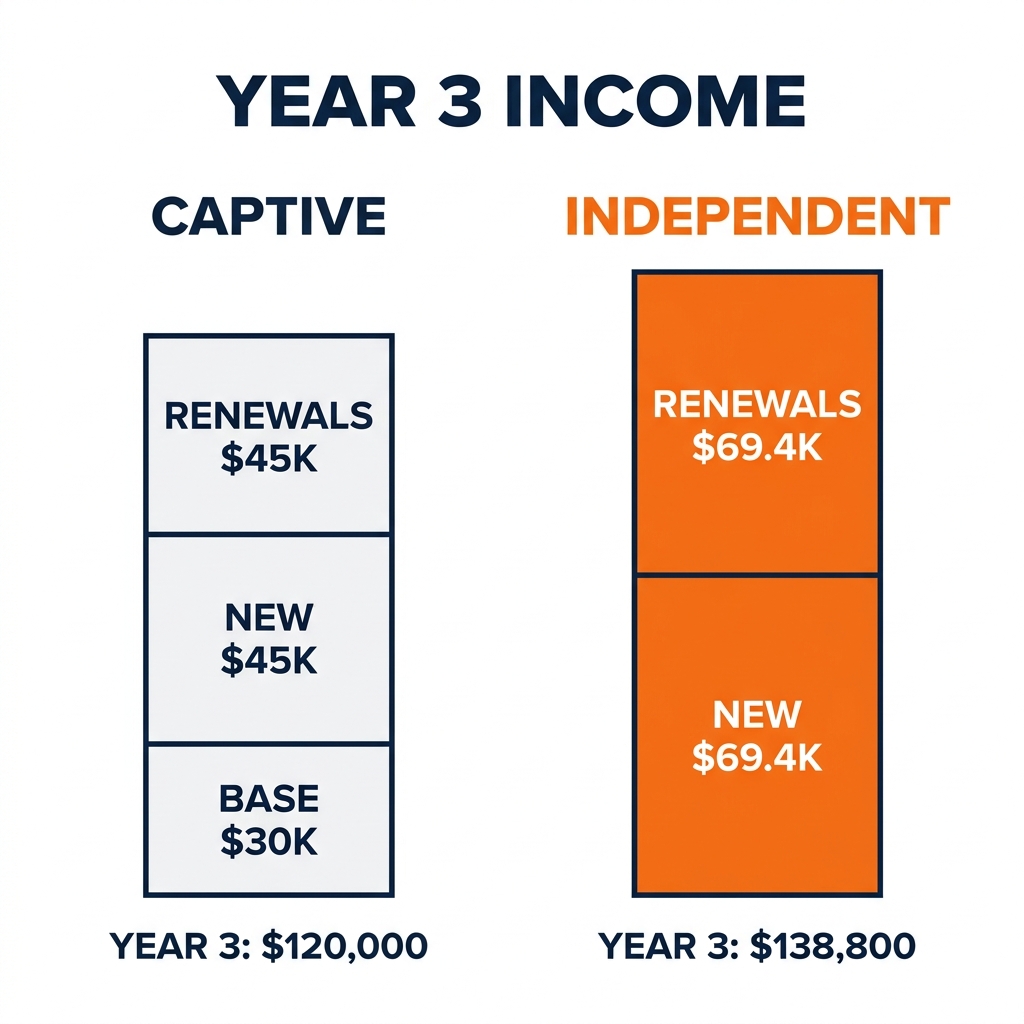

Captive Agent in Year 3

Income breakdown:

- Base salary: $30,000

- Year 3 new business: 100 × $450 = $45,000

- Year 1 + Year 2 renewals (200 active clients × $225): $45,000

- Total Year 3 income: $120,000

That's a real number. Stable, predictable, with leads coming from the company.

The catch is what the next page of the spreadsheet doesn't show. If the agent leaves in year 4, the $45,000 in renewal income stops. The book stays with the company.

Independent Agent in Year 3

Income breakdown:

- Year 3 new business: 100 × $694 = $69,400

- Year 1 + Year 2 renewals (200 active clients × $347): $69,400

- Total Year 3 income: $138,800

Roughly $19,000 more in year 3 alone. The bigger story is what's underneath that number.

The independent agent owns the book. If they stop writing new business in year 4, they still collect $69,400 a year in renewals. If they keep writing, year 4 adds another renewal layer on top. By year 5, renewals alone can hit six figures.

That's the part of the Medicare agent commission split a captive contract can't replicate.

What Most Agents Get Wrong About Going Independent

The agents who struggle in the switch make the same three mistakes.

They underestimate year 1. Independent year 1 income is usually lower than captive year 1. Most agents need 6 to 12 months to rebuild lead flow, finish carrier appointments, and replace the support layer they just left. The income dip is real and short-term agents quit before it pays off.

They overestimate the platform cost. A full P&C-style independent agency launch can cost $40,000 to $60,000 to stand up. A Medicare-only independent practice is far cheaper. CRM, E&O, ad budget, and licensing costs run a fraction of that. Most agents do not need a brick-and-mortar office or a staff of five.

They underprepare for lead generation. Captive agents get leads handed to them. Independents have to build the lead engine themselves. This is where most failed transitions actually fail. It's not the contract or the commission. It's that the agent never built the pipeline to feed the contract.

What You Need Before You Make the Switch

Five things in place before going independent insurance agent:

- Carrier appointments. Apply for at least 3 to 5 MA carriers and 2 to 3 final expense carriers. Allow 60 to 90 days.

- An FMO contract. This is your hierarchy partner. Pick one that pays street level and offers tech and training, not just paperwork.

- A CRM with automation. GoHighLevel is the standard for Medicare independents. Lead routing, SMS sequences, calendar booking, all in one place.

- A 6-month income runway. Cover 6 months of personal expenses while the pipeline builds. This is what kills most transitions if it isn't in place.

- A lead generation plan. Not "I'll figure it out." A plan. Whether it's exclusive leads, paid ads, referrals, or a mix, it has to be defined before you turn off the captive paycheck.

About half of independent Medicare agents who stick with the business 5 or more years end up earning over $100,000 annually. The ones who hit that number all have these five pieces in place. For a step-by-step framework on building each piece, see our guide on how to scale your Medicare agency in 2026.

Independent Medicare Agent Income Compounds, But Only If the Pipeline Is Built

The independent vs captive Medicare agent income gap in year 3 isn't huge in dollar terms. The compounding gap by year 5 and year 10 is enormous. And the book ownership gap is permanent.

The agents who win this comparison are the ones who solve lead generation before they solve commission rates. A 100% commission split on 0 leads is still 0 dollars.

Ready to see what consistent Medicare lead flow looks like for your market? Book a free 20-minute strategy call here. No pitch. Just a look at your market and what consistent leads could look like.

Not ready for a call? Take the free 60-second Medicare Lead Gen Roadmap assessment. It shows you exactly where your pipeline can grow.

Frequently Asked Questions

Q: How much more does an independent Medicare agent make than a captive agent?

A: Independent Medicare agents earn 33% to 50% more per enrollment than captive agents. Year 1 income often looks lower for independents because of startup costs and pipeline ramp. By year 3, the renewal compounding plus the higher commission rate puts independent income $15,000 to $25,000 ahead per year, and the gap widens after that.

Q: How long does it take to make money as an independent Medicare agent?

A: Most independent Medicare agents see an income dip for 6 to 12 months while the pipeline builds and carrier appointments finalize. Year 2 typically matches or exceeds prior captive income. By year 3, the renewal stack from years 1 and 2 starts adding meaningful residual income on top of new business.

Q: Do independent Medicare agents own their book of business?

A: Yes. An independent Medicare agent owns the client relationship and the renewal stream. Captive agents almost always sign contracts where the carrier or parent agency owns the book, which means renewals stop the day the agent resigns. Book ownership is the single biggest financial difference between the two models.

Q: What does it cost to leave a captive Medicare contract?

A: The direct cost is usually low. The hidden cost is the lost renewal income on the book you built while captive. Some contracts also include non-compete or non-solicit clauses that limit which clients you can move with you. Read the contract before you sign anywhere new and consider a 6-month income runway to bridge the transition.