Medicare Agent Commission Rates 2026: Which Plan Pays Most?

Medicare agent commission rates for 2026 just went up. CMS raised the maximum Medicare Advantage cap by nearly 11% in most states, making this the best year in recent memory to build a Medicare book of business.

But commission rates alone do not tell the full story. The agents who earn the most are not the ones selling the highest-commission plan. They are the ones who know which plans to stack, in what order, and how to maximize day-1 value and long-term renewals at the same appointment.

Medicare Agent Commission Rates in 2026: What CMS Changed

Every year, CMS releases the maximum Fair Market Value that Medicare Advantage organizations can pay independent agents and brokers. For 2026, those caps increased significantly for most of the country.

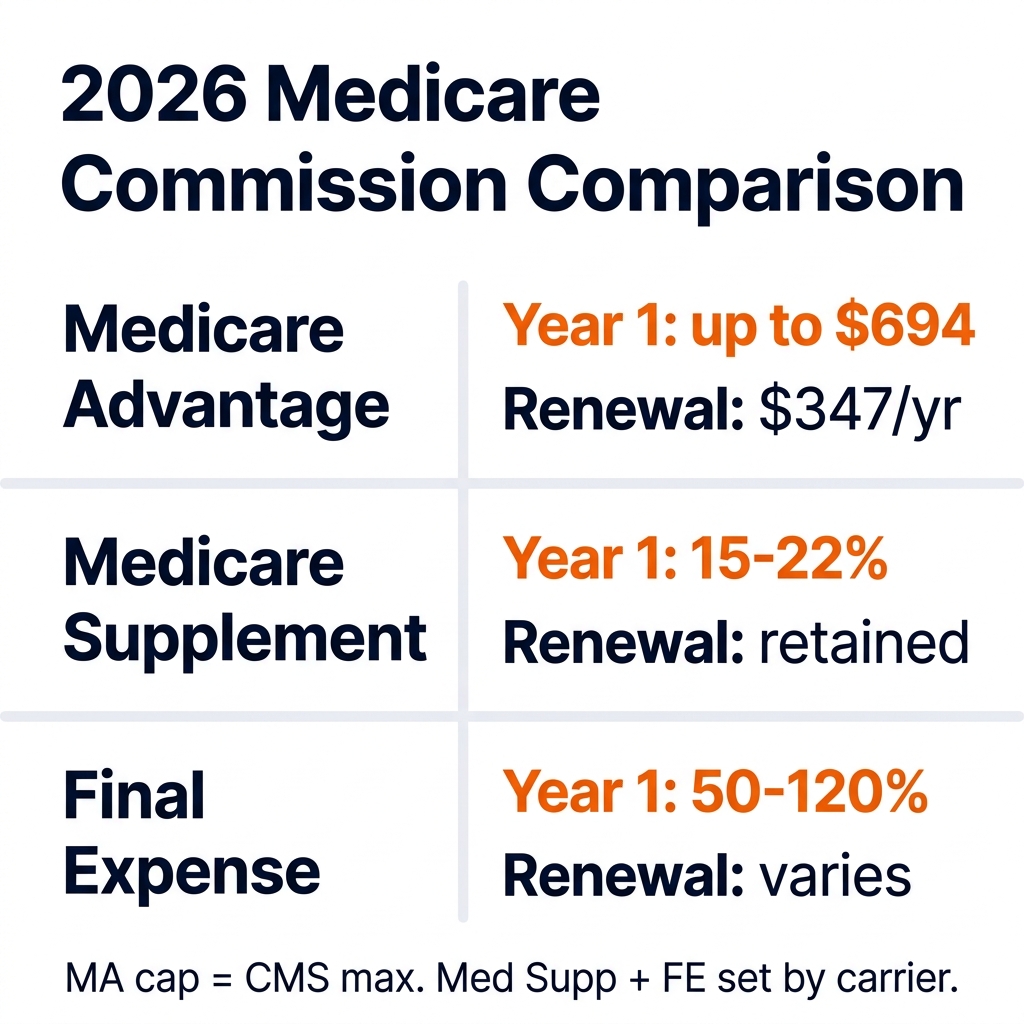

In most states, the 2026 initial Medicare Advantage commission cap is $694 per member per year, up from $626 in 2025. That is a 10.9% increase year over year. Renewal commissions for most states increased to $347 per member per year, up from $313.

These are the CMS maximums. Actual commissions depend on your carrier contracts. Some carriers pay the full cap. Some pay less. Contract directly with carriers or through an FMO to see what they actually pay in your market.

Why the Increase Matters for Your Book

A 10.9% jump in both initial and renewal commissions is meaningful. At scale, it changes the math on your book. An agent with 100 active MA clients earns $34,700 in renewals alone at the 2026 renewal rate ($347 x 100).

That is before any new enrollments. Before cross-sells. Before FE or Supplement income. The renewal floor is rising, and that compounds over time.

Medicare Advantage Commission Rates: Year 1 vs. Renewal

MA is the foundation of most Medicare agents' income for one reason: the renewal stack. You write a client once and collect a commission every year they stay enrolled.

At 2026 rates, a single MA enrollment is worth up to $694 in year 1, then up to $347 per year every year after. Over five years, that one client is worth up to $2,082 in commissions alone ($694 + $347 x 4 = $2,082).

That long-term income is why MA is the core product in every serious Medicare agent's business. The first-year number looks modest. But it is the renewal stack that builds income you can predict and depend on.

The Renewal Stack in Practice

Here is what building a book of 100 MA clients looks like at 2026 rates:

- Year 1 per new enrollment: up to $694

- Year 2+ per enrolled client: up to $347/year

- 100-client book at 2026 renewal rates: up to $34,700/year recurring

- 5-year value per client (initial + 4 renewals): up to $2,082

These are CMS cap figures. Actual earnings depend on carrier contracts and retention. But the structure is what matters: MA is a recurring income product disguised as a one-time sale.

Medicare Supplement Commission Rates

Medicare Supplement commissions are not capped by CMS. Each carrier sets its own structure. Most pay 15-22% of the annual premium in year 1, with renewal commissions that vary by carrier.

The first-year payout on Med Supp can be significant, especially on Plan G and Plan N policies where premiums are higher. The trade-off is that Med Supp clients are often more price-sensitive and more likely to switch carriers at renewal, which affects your retention.

Med Supp vs. MA: How to Choose

Most agents sell both, and route clients to the right product based on their situation. Original Medicare with a Supplement is the right fit for some clients. An MA plan fits others. Knowing the difference, and being able to write both, is what separates income-capped agents from income-stacked ones.

The LTV on a retained Med Supp client is $1,500 or more over their lifetime, which is comparable to a retained MA client at current rates. The key word is retained. Your retention system matters as much as your commission rate.

Final Expense Commission Rates: The Day-1 Multiplier

Final Expense (FE) is where agents earn the highest first-year commission of any Medicare-adjacent product. Most FE carriers pay 50-120% of the annual premium in year 1. On a $600 annual premium policy, that is $300-$720 in first-year commission.

The reason FE matters for Medicare agents specifically is timing. You are already sitting with a 65-year-old who just enrolled in a Medicare plan. They are in an insurance mindset. They have been thinking about their coverage. FE is the natural next conversation.

The Cross-Sell That Changes Your Day-1 Value

Adding FE to a Medicare appointment is the single fastest way to raise your day-1 close value. The benchmark for agents we work with is $900-$1,500 at the first appointment, including cross-sells written the same day.

That number does not happen by accident. It requires having FE carriers contracted, a short bridge from the Medicare conversation to the FE conversation, and a consistent script for introducing it. Agents who do this consistently do not have $300 appointments. They have $900 appointments.

You can see how the cross-sell path compounds over a client's lifetime in the Medicare cross-sell household LTV breakdown.

PDP Commission Rates: Small but Required

Prescription Drug Plan (PDP) commissions are modest: $100 in year 1 and $50 per year at renewal. Many agents skip PDP or treat it as an afterthought.

That is a mistake for two reasons. First, you are already helping the client with their Medicare coverage -- PDP is part of the full picture, and writing it yourself keeps the client in your book. Second, at scale, $50 per client per year adds up. A book of 200 PDP clients pays you $10,000/year in renewals without any extra effort.

Which Medicare Plan Type Pays the Most in 2026?

The right answer is: all of them, stacked in the right order at the right appointment. Here is how the income math works when you sell multiple products:

- MA: Up to $694 year 1, $347/year renewal -- long-term income engine

- Med Supp: 15-22% first-year -- higher upfront % but not capped by CMS

- FE: 50-120% first-year -- highest upfront payout, best cross-sell at Medicare appointment

- PDP: $100 year 1, $50 renewal -- small but adds up across a full book

The agents hitting $30,000+/month in Medicare commissions are not just selling more MA plans. They are writing FE at the same appointment, retaining clients for renewals, and working a cross-sell path that stacks income across products over time.

If you want to understand what that growth path actually looks like at the unit level, the guide to scaling your Medicare agency walks through the system behind it. For the full breakdown of how MA client value compounds across a household, see the Medicare lead generation system that feeds the book.

Build the Income Stack, Not Just the Enrollment Count

Medicare agent commission rates in 2026 are the highest they have been in years. The MA cap increase means your book is worth more per client than it was 12 months ago.

But the real income lever is not the rate. It is the stack. MA renewals for the floor. FE for the day-1 multiplier. Med Supp for the premium clients. PDP to retain the full relationship.

The agents who master this stack do not grind harder. They earn more from the same number of appointments.

Not sure how your current Medicare lead pipeline stacks up against the benchmark?

Take the free 60-second assessment and get your personalized Medicare Lead Gen Roadmap. It shows you where your pipeline is strong and where it is costing you income.

Get Your Free Medicare Lead Gen Roadmap

Or if you are ready to talk through your market and what a consistent pipeline looks like, book a free 20-minute strategy call. No pitch. Just a look at the numbers.

Frequently Asked Questions

Q: What are the Medicare Advantage commission rates for 2026?

A: In most states, the 2026 CMS maximum initial commission is $694 per member per year, and the maximum renewal commission is $347 per member per year. These are caps set by CMS -- actual commissions depend on your carrier contracts, which may pay the full cap or less. Rates vary by region; some high-cost states like California and New Jersey have different caps.

Q: How much does a Medicare Supplement agent earn per enrollment?

A: Medicare Supplement commissions are not capped by CMS. Most carriers pay 15-22% of the annual premium in year 1. The exact dollar amount depends on the plan type and premium level. Med Supp LTV is $1,500 or more per retained client.

Q: How do Final Expense commission rates compare to Medicare Advantage in 2026?

A: Final Expense pays the highest first-year commission of any Medicare-adjacent product, typically 50-120% of the annual premium. Medicare Advantage pays up to $694 in year 1 at 2026 CMS cap rates, but builds a renewable income stack of up to $347 per client per year. Most agents sell both and cross-sell FE at Medicare appointments to maximize day-1 close value.

Q: Which Medicare plan type pays the most commission long-term?

A: Medicare Advantage is the strongest long-term income builder because of the annual renewal structure. At 2026 rates, a single MA enrollment is worth up to $2,082 over five years. Stacking MA with Final Expense cross-sells at the appointment produces the highest combination of day-1 income and long-term renewal revenue.