Medicare Client Lifetime Value: The 5-Year Math

Medicare client lifetime value is the single number that decides whether your agency grows or stalls. Most agents track CPL and close rate. The agents who scale track LTV. One MA enrollment compounds into $2,082 over 5 years. Stack the right cross-sells and it crosses $2,700.

What Medicare Client Lifetime Value Actually Means

Medicare client lifetime value is the total commission a single enrollment pays you across the full life of the client relationship. It is not the day-1 payout. It is the 5- or 6-year revenue you earn from one enrollment plus everything you cross-sell to that same household.

CMS structures Medicare commissions on a 6-year cycle. You collect a Year 1 commission, then renewals every year the client stays on the plan. The 6-year cycle was confirmed in the 2026 Ritter Insurance Marketing commission update.

Most agents underprice their book because they only see the first payment. The renewal stack is where the real income lives.

Why This Number Decides Your Strategy

If a Medicare client is worth $500 to you, a $50 CPL feels expensive. If that same client is worth $2,700, a $50 CPL is a rounding error. The math changes how you spend on leads, how you build your team, and how you measure agent performance.

LTV also decides which leads are worth fighting for. A T-65 hand-raised lead converts to a multi-product household. A shared aged lead barely converts at all. The difference shows up in your 5-year book value, not your weekly enrollment count.

The Base Math: One Medicare Advantage Client Over 5 Years

Here is the floor math. One MA enrollment with no cross-sells, retained for 5 years.

Year 1 Commission

For 2026, the national maximum MA commission is $694 per enrollment. That is up from $626 in 2025. This is the day-1 payout you collect when the policy goes effective.

Renewal Income, Years 2 Through 5

You collect a $347 renewal each year the client stays on the plan. That is also up from $313 in 2025. Across years 2, 3, 4, and 5, you stack 4 renewals.

The math: $694 + (4 × $347) = $694 + $1,388 = $2,082 in 5-year Medicare LTV per client.

Why the 6-Year Cycle Matters

Every Medicare client you enroll is a 6-year revenue commitment from CMS. If you keep the client on the plan, you collect every renewal year. If they switch carriers but stay your client, you still collect renewals at the lower rate. This is recurring revenue most insurance agents do not realize they have.

Agents who lose clients lose 4 to 5 years of $347 renewal commissions per loss. That is why retention is more valuable than acquisition once your book passes 100 clients.

How Cross-Selling Doubles Your Medicare Client Lifetime Value

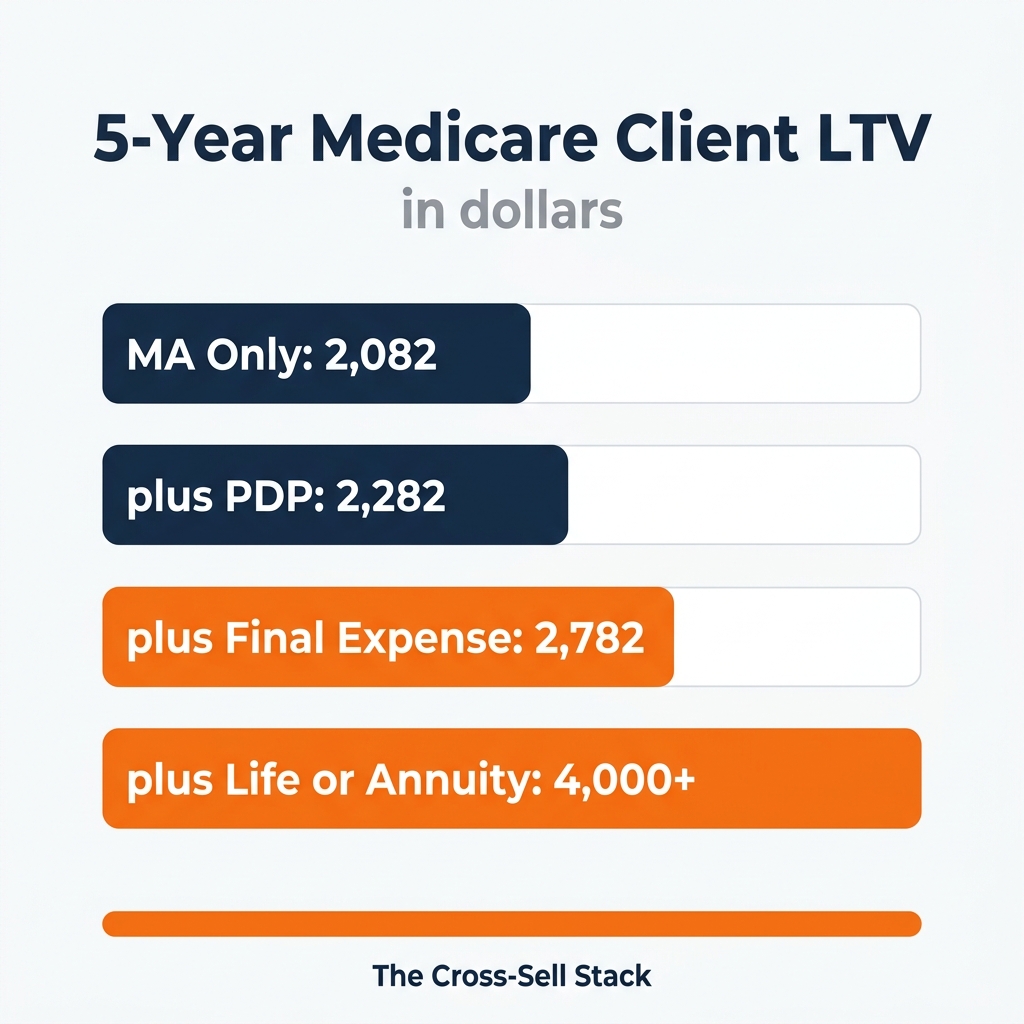

The $2,082 number is just the MA piece. Real Medicare client lifetime value compounds when you cross-sell into the household. The cross-sell path that works is MA, then PDP, then Final Expense, then Life or Annuity.

Adding PDP

A Medicare Advantage client without a drug plan is rare. Most MA-PD plans bundle the drug coverage in. But standalone PDP enrollments still pay separate commissions.

PDP pays roughly $100 Year 1 and $50 renewal. Realistic 5-year PDP LTV is about $200 once you factor in plan switching. That brings your stacked LTV to $2,082 + $200 = $2,282.

Adding Final Expense

This is the lever most agents miss. Every senior on Medicare is a final expense candidate. The conversation is natural. You are already discussing end-of-life planning, prescriptions, and medical events.

A typical FE policy at $50 per month produces a $600 annual premium. Year 1 commission is 50 to 120 percent of premium depending on carrier. Call it $400 to $700 in Year 1 alone. Stack modest renewals and FE adds another $500 or so over 5 years. That moves your LTV from $2,282 to roughly $2,700 to $2,800 per client.

That is how you hit the benchmark.

Adding Life or Annuity

The highest-LTV agents stack a life or annuity sale on top. A modest term life policy or a small annuity rollover can add $1,000 to $3,000 in additional commission. Now your client is worth $4,000 to $5,000 over 5 years.

This is the same client. Same lead cost. Same hour of relationship-building. The product stack is what changes the math.

Why Agents Who Track Medicare Client Lifetime Value Beat Agents Who Track CPL

CPL tells you what you spend. LTV tells you what you earn. Agents who only track CPL chase cheap leads. Agents who track Medicare client lifetime value chase profitable leads.

A $30 CPL on shared leads with a 3 percent close rate produces a $1,000 cost per enrolled client and a 50 percent MA-only client. Net 5-year LTV: $2,082 minus $1,000 = $1,082 per client.

A $50 CPL on exclusive hand-raised leads with a 20 percent close rate produces a $250 cost per enrolled client and a much higher cross-sell rate. Net 5-year LTV with cross-sells: $2,700 minus $250 = $2,450 per client.

Same agent, same products, completely different agency. The lead source changes the LTV.

This is why we built the 30-Day Medicare Lead Sprint around exclusive SMS-verified T-65 leads. We guarantee 25 exclusive T-65 leads in 30 days, delivered only to you. The lead quality is what gives the cross-sell math a chance to compound.

How to Build a Book Worth $2,700+ Per Client

Three habits separate agents at $1,000 LTV from agents at $2,700+ LTV.

1. Track Medicare Client Lifetime Value Per Enrollment

Most agents track monthly revenue. Top agents track LTV per client cohort. Build a simple spreadsheet. For every enrollment, log carrier, product, premium, and cross-sells. Review quarterly. You will find which lead sources, which campaigns, and which referral partners produce $2,700+ households versus $1,000 single-product enrollments.

2. Build a Cross-Sell Sequence Into Your Process

Cross-selling does not happen by accident. Build it into your client process. After the MA enrollment, schedule a 30-day follow-up. That call is your FE conversation. Six months in, that is your annuity or life check-in. Top agents have a mapped sequence. Average agents wait for the client to bring it up.

For the full cross-sell sequencing playbook, see our Medicare cross-sell map. It covers timing, scripts, and which product comes next.

3. Protect Retention Like It Is Your Revenue

Because it is. Each lost client costs you 4 to 5 years of $347 renewals. Annual benefit reviews during AEP, birthday calls, and proactive plan check-ins are how you keep clients in your book. A 90 percent retention rate compounds. A 75 percent retention rate bleeds.

This is the lever that turns a high-LTV book into a scalable agency. For the full picture on building a system that supports this, read how to scale your Medicare agency.

Why Medicare Client Lifetime Value Changes Your Whole Business

When your client is worth $1,000, you run a transactional business. You sell, you move on, you start over each AEP. When your client is worth $2,700, you run a relationship business. You sell once, you serve for 5 years, and your renewals fund next year's acquisition spend.

That is the difference between an agent who grinds and an agent who builds a book. Medicare client lifetime value is the metric that forces that shift.

Want to see how exclusive T-65 leads change your Medicare client lifetime value math?

We put together a short video that walks through the whole system. How the leads are generated. How they are qualified. How a 25-lead Sprint compounds into a $35,000+ book over 5 years when the cross-sell stack is in place.

Frequently Asked Questions

Q: What is a Medicare client worth over 5 years?

A Medicare Advantage client retained for 5 years is worth $2,082 in MA commissions alone ($694 Year 1 plus 4 × $347 renewals). When you add PDP, final expense, and life or annuity cross-sells, the same client crosses $2,700, and often reaches $4,000+ for fully cross-sold households. That is the real Medicare client lifetime value most agents underestimate.

Q: How do you calculate Medicare client lifetime value?

Calculate it product by product. Year 1 commission plus renewal income for each year the client stays on the plan, then stack every cross-sell. For 2026 MA: $694 Year 1 plus ($347 × number of renewal years). Add PDP, FE, life, and annuity commissions to that base. Then subtract acquisition cost to get net LTV.

Q: How much do Medicare agents earn per client over time?

An MA-only client retained 5 years pays $2,082 in 5-year Medicare LTV. An MA + PDP + FE client crosses the $2,700 benchmark. An MA + PDP + FE + annuity client reaches $4,000 to $5,000. The product stack is the biggest lever in Medicare agent recurring income.

Q: Does cross-selling really double Medicare LTV?

Cross-selling does not always double LTV, but it consistently adds $500 to $2,500 per household. Adding final expense alone moves an MA client from $2,082 to roughly $2,700 over 5 years. Adding a small annuity or term life on top can push a single household to $4,000+. The cross-sell stack is how top agents compete with cheap-lead operators. They earn 2 to 3x more per client without buying more leads.